This year has witnessed further technical developments, such as ChatGPT, and political ones, like the increasing formation of geopolitical blocks. This has also affected the evolution of the payment segment, where new trends are emerging as follows.

Availability of financial services in the customer checkout process.

Description of the trend

Embedded finance refers to digital payment options embedded within non-payment apps. More widely available across multiple consumer touchpoints, they add financial services offerings within customer checkouts enabling corporates to intuitively cross- and upsell products and services.

Provision of financial services will be made available in existing physical and digital checkout flows. (e.g., embedded banking, payments, insurance, investment, lending, loyalty).

Added value

Efficient standard processes

Highly customizable

Low operational costs

Customer-centric offers & problem solving

Data-driven approach

Availability of financial services in the customer checkout process.

Description of the trend

Embedded finance refers to digital payment options embedded within non-payment apps. More widely available across multiple consumer touchpoints, they add financial services offerings within customer checkouts enabling corporates to intuitively cross- and upsell products and services.

Provision of financial services will be made available in existing physical and digital checkout flows. (e.g., embedded banking, payments, insurance, investment, lending, loyalty).

Merchants establish internal regulated speed boats to push innovative and convenient services.

Description of the trend

Merchants integrate with their own internal payment service provider and own their technology and banking license – potentially also in addition to the existing inhouse bank/-s.

Internal teams are required for reporting and general management.

Added value

High individualization

Best user convenience for consumers

High flexibility

New solution offerings

Merchants establish internal regulated speed boats to push innovative and convenient services.

Description of the trend

Merchants integrate with their own internal payment service provider and own their technology and banking license – potentially also in addition to the existing inhouse bank/-s.

Internal teams are required for reporting and general management.

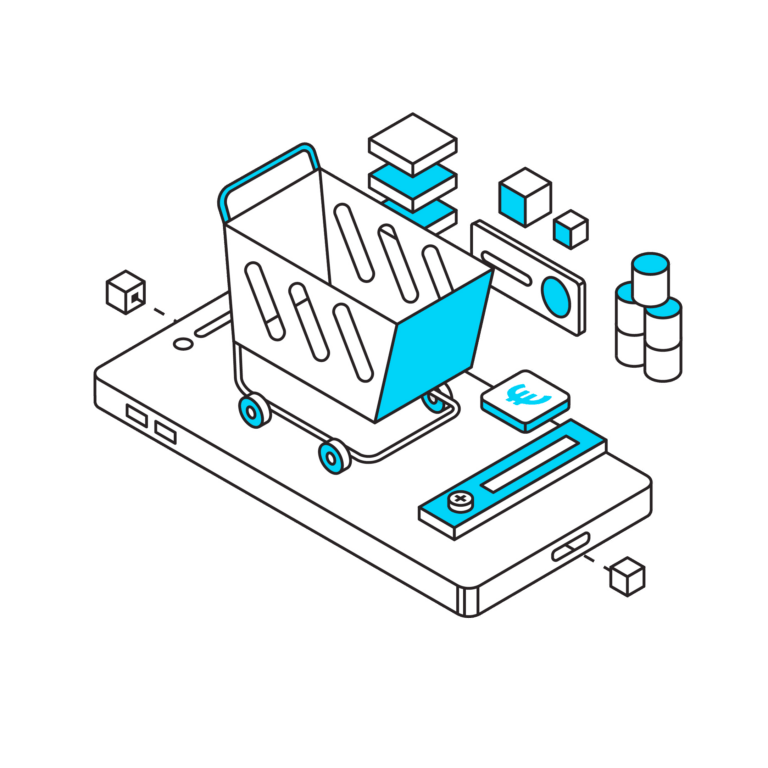

Companies with online and offline stores, offer its shoppers the opportunity to buy items from the online inventory directly at the physical points of sale , offering a unified payment solution.

51% expect the share of sales from physical stores to increase in the next year BUT stores need to offer more than just products and services that are also available online. Technology plays a critical role in creating an in-store experience worth visiting.

Added value

Physical shop as up- und cross-selling opportunities

Better customer experience

More freedom & choice for customers

Greater product offer without logistical problems

A step forward in the omnichannel approach.

Description of the trend

Companies with online and offline stores, offer its shoppers the opportunity to buy items from the online inventory directly at the physical points of sale , offering a unified payment solution.

51% expect the share of sales from physical stores to increase in the next year BUT stores need to offer more than just products and services that are also available online. Technology plays a critical role in creating an in-store experience worth visiting.

Added value

Physical shop as up- und cross-selling opportunities

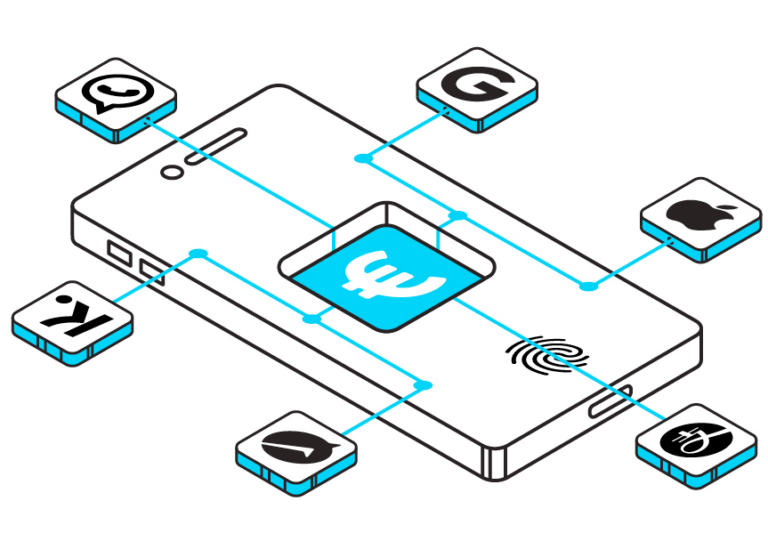

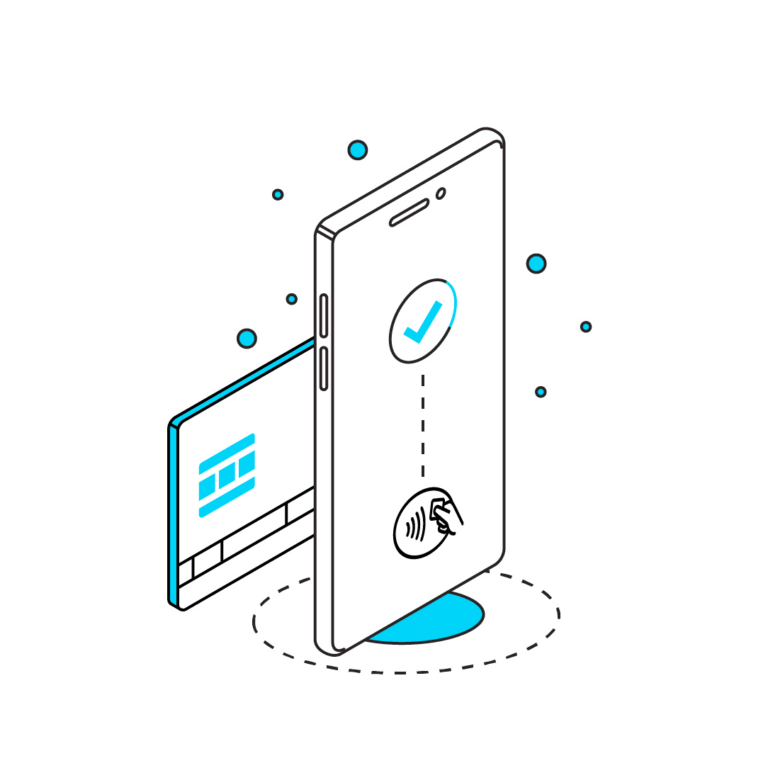

Accept contactless payments directly on a smartphone.

Description of the trend

Tap to Pay or SoftPoS technology enables secure payments between a traditional card or digital wallet and an NFC-enabled mobile device, without the need for any additional hardware.

Merchants can also benefit from SoftPos orchestration (white label SoftPoS app or incorporation of the technology into their existing solution).

34.5M merchants globally will use it by 2027.

Added Value

Easy maintenance and upgrades

Easy to use (smartphones to accept payments)

Cost-effective

Higher use of contactless payments

Accept contactless payments directly on a smartphone.

Description of the trend

Tap to Pay or SoftPoS technology enables secure payments between a traditional card or digital wallet and an NFC-enabled mobile device, without the need for any additional hardware.

Merchants can also benefit from SoftPos orchestration (white label SoftPoS app or incorporation of the technology into their existing solution).

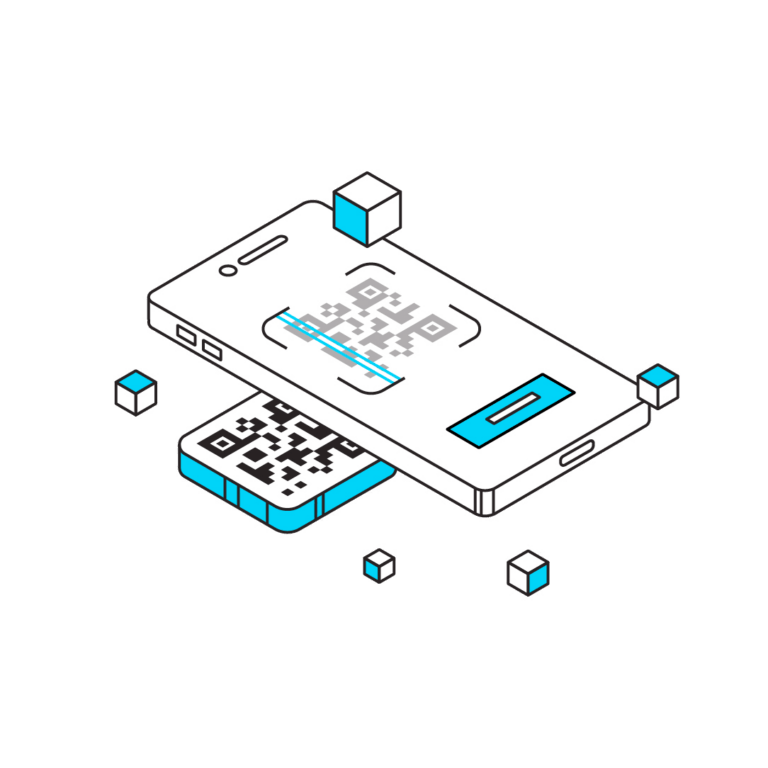

Quick Response (QR) code is a two-dimensional code capable of storing URLs or other information that can be accessed by the camera on a smartphone.

Depending on the code, the mobile device performs various tasks, including confirming payments. Mostly used in APAC and in e-commerce, QR codes are becoming successful also among retailers around the world for their simplicity and flexibility. QR codes are powerful assets for quickly redirect the customer to the payment platform without requiring the typing in of all data.

Market size will reach $35 bn by 2030.

Added value

Easy to use

Fast & convenient

Safe

Customer-friendly

Flexible, fast and precise.

Description of the trend

Quick Response (QR) code is a two-dimensional code capable of storing URLs or other information that can be accessed by the camera on a smartphone.

Depending on the code, the mobile device performs various tasks, including confirming payments. Mostly used in APAC and in e-commerce, QR codes are becoming successful also among retailers around the world for their simplicity and flexibility. QR codes are powerful assets for quickly redirect the customer to the payment platform without requiring the typing in of all data.