The world of payments is constantly changing, driven by advancing technology, changing consumer habits and regulatory developments. These dynamics have left their mark on the development of the payments sector, where new trends are emerging as follows.

Real-time settlements: Impact on the financial world

Instant payment is more than just a quick bank transfer; it represents a change in finance. With instant payments, funds can be sent and received in real time, regardless of the time of day or day of the week. Use cases such as P2P payments can therefore no longer only be offered by fintechs but can also be made accessible to the broad masses by banks.

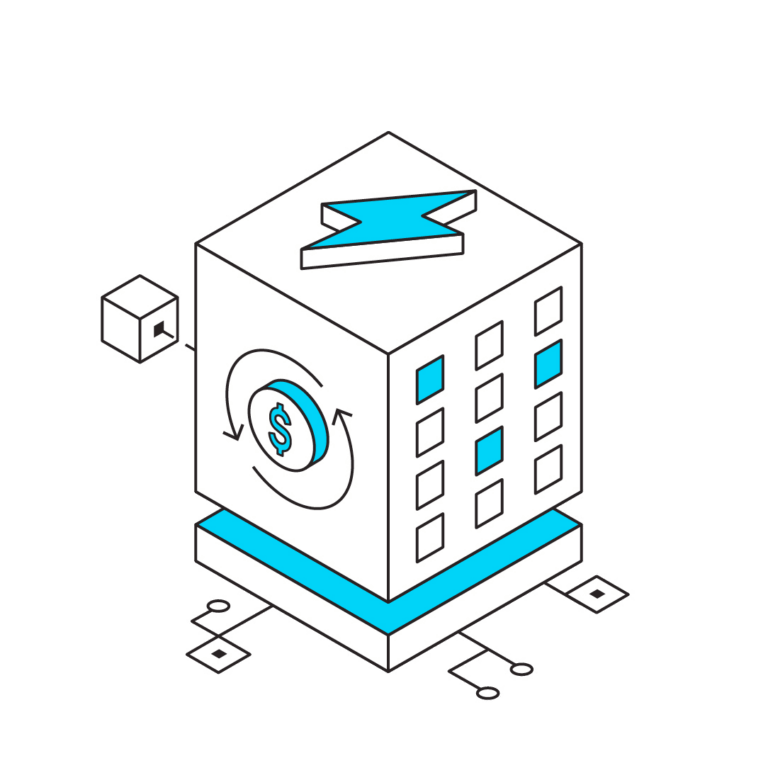

Payment orchestration is the efficient coordination of different payment service providers, methods and systems within a single platform to ensure seamless and optimized payment processes. Companies can react flexibly to the needs of their customers, regional requirements and changing market conditions. As part of payment orchestration, a central platform assumes the role of an orchestrator that controls and manages all payment processes. The functional, technical and regulatory components can be freely and flexibly combined from internal or external providers.

Added value:

Greater individualization

Internal & expert knowledge

Reduced dependencies

Centralization of all financial services within an efficient global platform

Speedboat to promote innovative financial services

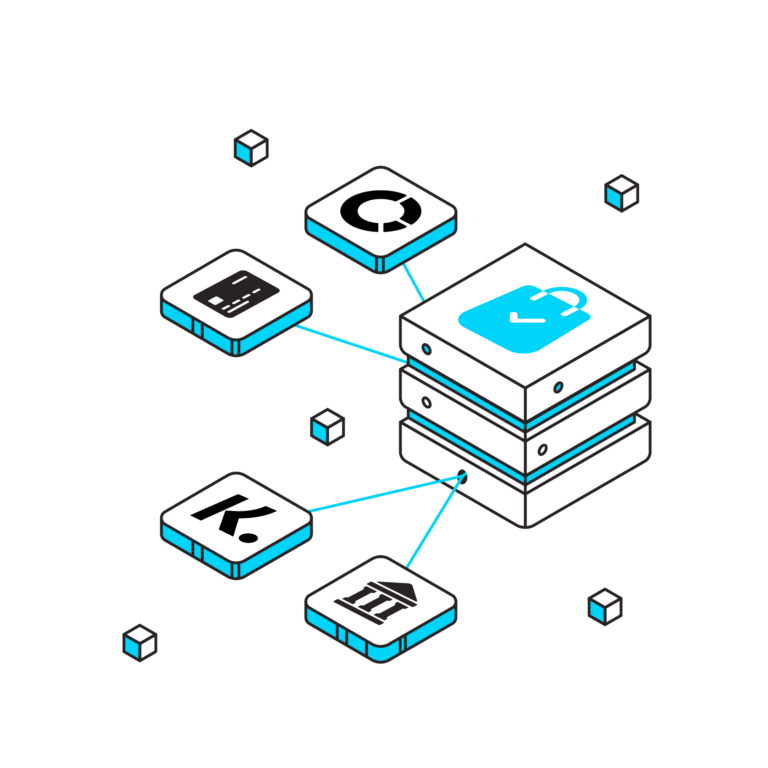

Corporate Fintech describes the bundling of all activities for digital payment processing in a legally independent company within a group. Companies become more agile and competitive by modernizing traditional financial processes and offering innovative solutions for the challenges of the modern economy.

The establishment of a Corporate Fintech is relevant for all companies that see digital payment processing as a strategic service of their company and want to position themselves accordingly.

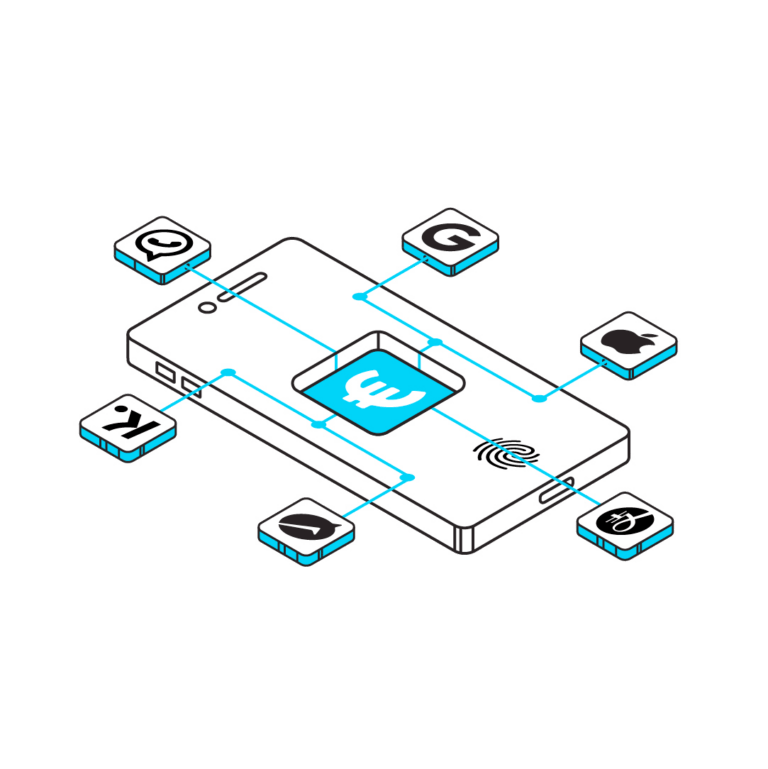

Social media as a new platform for digital payments

Integrating payment functions into social media makes the payment process simple and user-friendly. Users can send or receive money, make purchases and process donations directly via platforms such as Facebook, Instagram or Snapchat.

Social media platforms have expanded their e-commerce capabilities by integrating payment options directly into their core functions. This gives businesses the ability to sell products and services directly through their social media profiles, simplifying the entire purchasing process for customers.

Digital currencies are virtual or electronic forms of money that exist in the digital space. One well-known type of digital currency are cryptocurrencies, of which Bitcoin is the most well-known example. In contrast, central bank digital currencies (CBDC) are issued by central banks and are the counterpart to a country’s legal tender.

Digital currencies can help improve access to financial services, especially in regions where there is no traditional banking infrastructure. People without bank accounts can use digital currencies to send and receive payments, manage savings and participate in economic activities.

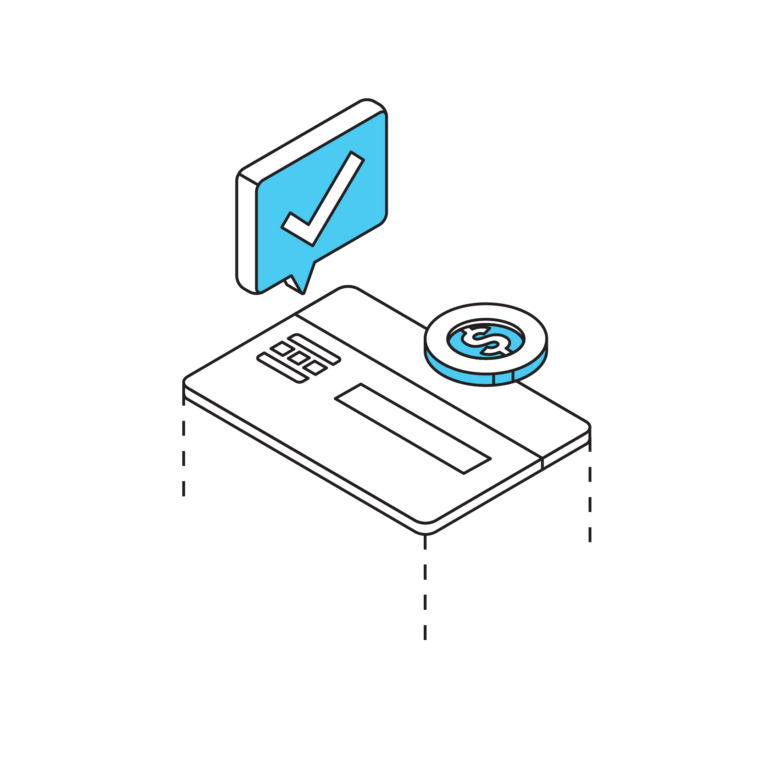

BNPL allows consumers to buy products or services immediately but pay the bill at a later point or split it into installments. This is particularly attractive in the higher-priced segment and for customers who do not have the means to pay the immediate purchase price.

The application process for BNPL is often simple and fast. In many cases, approval takes place in real time during the payment process. BNPL is often offered in online stores and on e-commerce platforms to increase the conversion rate and encourage customers to complete transactions.

Artificial intelligence is already making a decisive contribution to detecting and preventing payment fraud. By analyzing extensive data, AI models can make more informed decisions and minimize the risk of payment defaults.

AI is also used to create personalized payment experiences, to analyze customer preferences and behaviors to then provide individual recommendations for products or services and make the payment process more user-friendly.